Secondary Trading

From the beginning, we have been running Intercoin as a startup: building software people are willing to pay for and testing with real clients . We are passionate about building smart contract applications for communities worldwide and making crypto go mainstream. We want the ITR tokens to be sold to customers (projects, organizations and communities) who can use them in our products.

However, in crypto, there is a strong tradition of unrestricted secondary trading, and in fact this infrastructure can be helpful to allow tokens to be obtainable by customers in a decentralized manner. If we are to eventually transition to a decentralized system where people deploy Intercoin software the same way they can choose to run a web server or an Ethereum node, we’re going to need the tokens to be easily obtainable from more than one place.

Earlier this year, we have launched a version of ITR that is completely libre free-trading with no possible way for us to restrict the transfers. We’ve opened up a completely trustless way for existing holders of ITR to swap to this new version in limited quantities, and we may periodically suspend this ability in order to prevent flooding the open market with “whales”. Both forms of ITR have completely the same benefits, and are the same class of asset. Since the launch, some of our token holders have chosen to make the swap. The vast majority have chosen to hold their ITR for the long term.

One can make a parallel between this swap to libre ITR tokens and “removing the restrictive legend” on securities.

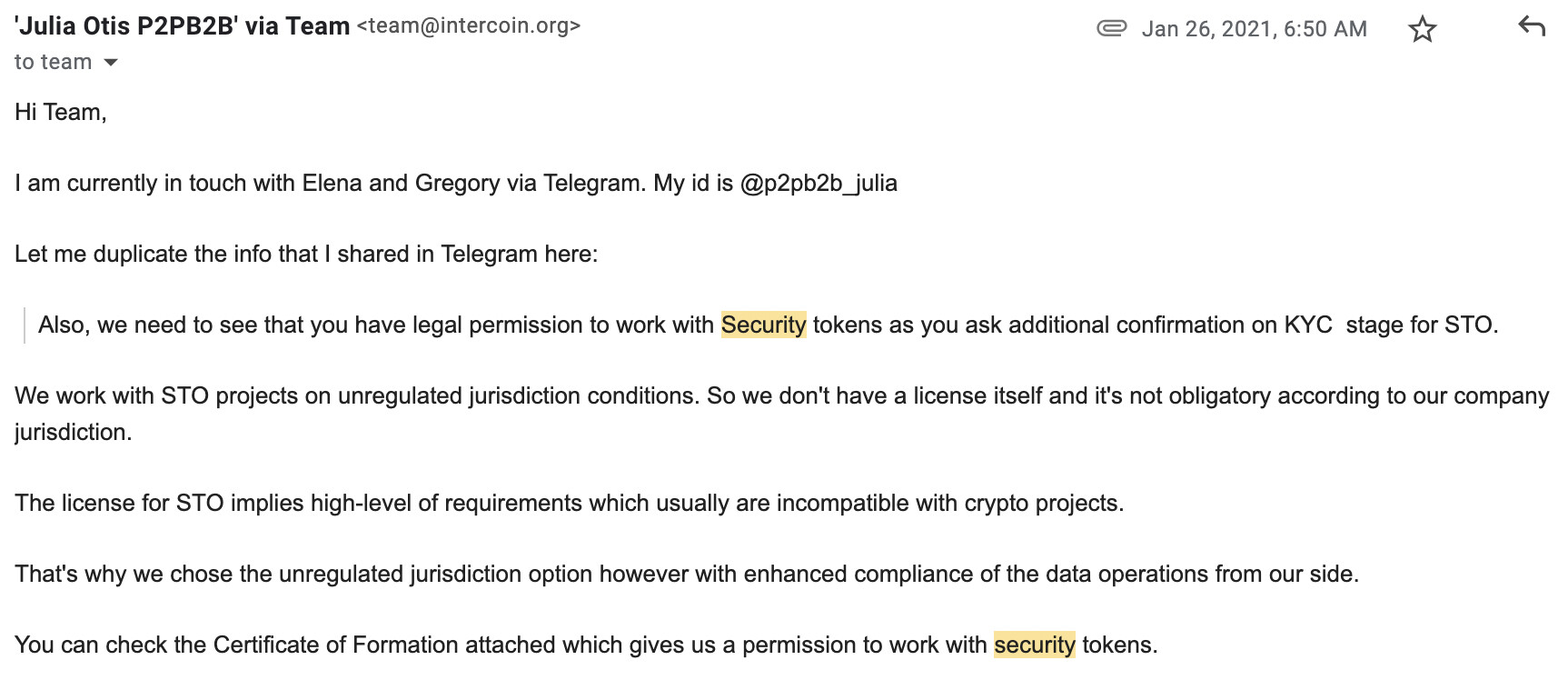

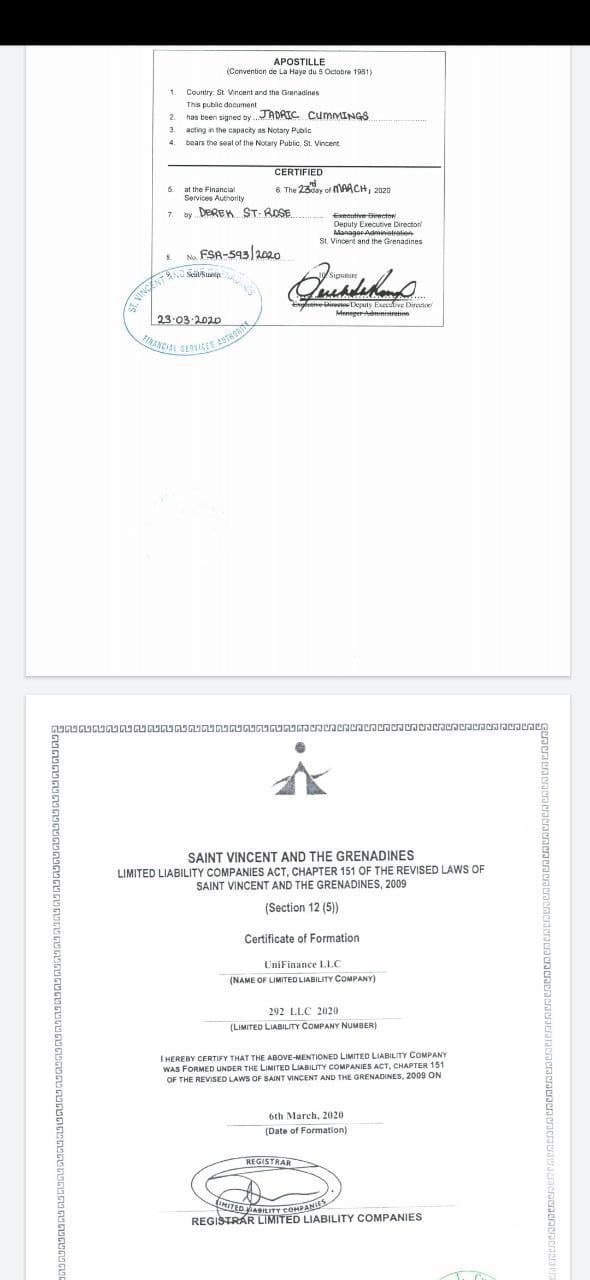

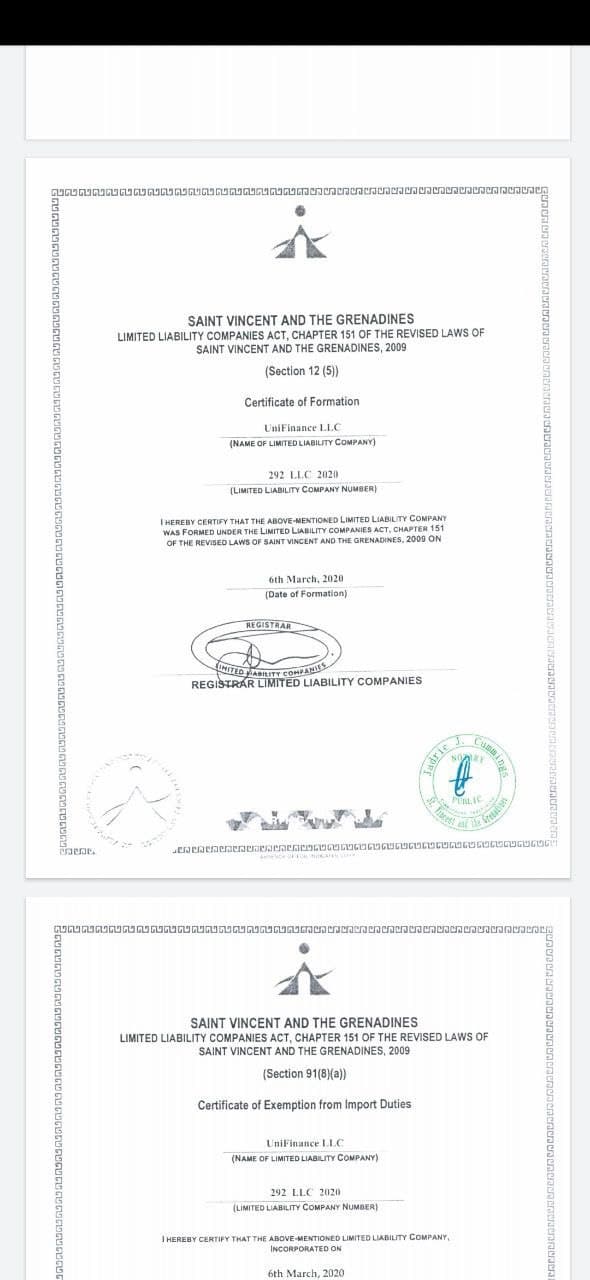

First ExMarkets, now P2P-B2B. Intercoin has 230 token holders which include original investors, team members, partners and many others. Some of them, including European investors, have been approaching non-US exchanges in order to list ITR. They take care of the logistics and listing fees.

The crypto industry has a dichotomy between “utility tokens” (e.g. to be used to pay for services) and “security tokens” (such as owning a share of real estate). In that dichotomy ITR tokens are designed to be utility tokens for our software and services, rather than security tokens as the industry commonly understands that term. However, just because a token has utility does not mean the SEC does not scrutinize the transactions under which it was originally sold, and consider those to be securities transactions that need to have been done under an exemption from registration. This is why we have always done our primary sales pursuant to exemptions such as Reg D, Reg S, and perhaps soon - Reg CF.

Non-US Exchanges

It’s an interesting situation. Earlier in the year, we were contacted by some of these exchanges, and we directly asked them regarding their regulatory ability to list tokens that may have been sold in transactions that may have originally been considered securities transactions in the USA. This is what they wrote back to us:

As a company, we ended up not pursuing listing on these exchanges. However, our token holders are now approaching exchanges like these, in order to list ITR on them. So far, the exchanges are not exactly top tier on the rankings, but it could be that some token holders are in talks with the higher ranked exchanges on the list. If and when they reach some sort of agreement, we encourage them to reach out to us if they want us to place additional links on our site letting people know of ITR’s availability. Adding the exchange feeds to CoinMarketCap and CoinGecko should likewise be done in cooperation with those sites, which have automated tools and rankings to vet these exchanges.

Decentralized Exchanges

Needless to say, some holders have already created liquidity pools on exchanges like UniSwap, which are completely decentralized. Many argue that decentralized exchange is a verb, not a noun, and since the contracts are immutable and not a “person” or an “institution” they are not covered under the idea of a “broker-dealer”. Indeed, we have seen many other technologies replace human operators:

- Voice Over IP has replaced Telephone Switchboard Operators, for instance, in routing long-distance calls, bringing costs down by orders of magnitude and ensuring a fair and efficient distribution (of audio/data packets around the world).

- Email has replaced the Post Office, to a large degree.

- The Web has disrupted magazines, newspapers, and so forth.

The open protocols underpinning the above transitions from manual operation to autonomous networks secured by multiple actors, have led to far better service and reliability for everyone. So it’s probably in regulators’ long term interest to allow the transition to trusted code bases, where smart contracts operating Liquidity Pools are produced from factories which have been heavily audited and battle-tested. When it comes to reliability and fairness could be considered superior to many centralized exchanges, without requiring oversight. Wash trading, for instance, would be harder to do when trading fees are relatively high for everyone without exception. There would be no information asymmetry between an exchange operator and its participants.

Marketing

There has also been interest from holders of ITR in marketing the Intercoin tokens to the public, engaging crypto influencers, etc. Some have reached out and asked us if they can target their advertisements to people outside the USA, such as location-based targeting on Facebook and Google. While we cannot control their actions, we do insist on two major things:

-

That they review local laws and mores of the jurisdictions and platforms where they will be advertising

-

That any advertising contain absolutely true, fact-checked information rather than exaggerations, outright fabrications, or even forward-looking statements presented as fact. Better to stick to what has already been done, and reference the site and the growing amount of information publicly presented here

-

If influencers are being paid in ITR tokens, they should consider disclosing that. Typically, it is actually reassuring (good optics) that an influencer chose to be paid in the token they’re talking about, showing they believe in its potential rather than just currencies that are already established (ETH, BTC, GBP etc.) As far as US regulations, as long as whomever is paying this influencer is not an issuer, underwriter or dealer, Section 17b disclosures do not need to apply.

Furthermore, US regulations may not necessarily apply if the advertisements are solely being delivered in areas outside the United States, such as this humble DOGELON advertisement in London

It is becoming increasingly common for holders of cryptocurrencies to pay for public advertising campaigns for those cryptocurrencies. This is often true of memecoins, such as the DOGEcoin superbowl ad and Floki Inu on buses in London! Notice, however, that this is still unusual and local advertising watchdog organizations have looked into these ads. They often look for advertising to be responsible, something that goes beyond merely 2 and 3 above, and considers informing the public of the risks of buying volatile assets, as we have done in our offering memorandum whenever we undertook to sell ITR through our website.

What’s Next

For the Intercoin ecosystem to ever become truly decentralized, tokens like ITR should be obtainable from a variety of places. Perhaps the most straightforward such place is smart contracts on the blockchain, powering decentralized exchanges such as Bancor and UniSwap, PancakeSwap and its ilk.

However, another mechanism by which to get the tokens into the hands of the public can include crowdfunding platforms, such as Republic.co in the USA which has already democratized access to some crypto token offerings, and other crowdfunding platforms may follow suit. That should be an interesting place.

Ultimately, though, we expect the DeFi ecosystem to mature and increasingly replace the centralized exchanges which require oversight and regulation to curb the kind of unpredictable, secretive or self-interested behavior that properly audited smart contracts would simply not be capable of. And just like with other technology replacing human operators, we as a society will eventually come to rely on them, just as we rely on the Internet to route our voice calls instead of telephone switchboard operators. Then the regulators wouldn’t need to work so hard to ensure reliable systems – the technology and standards would already do it for us.